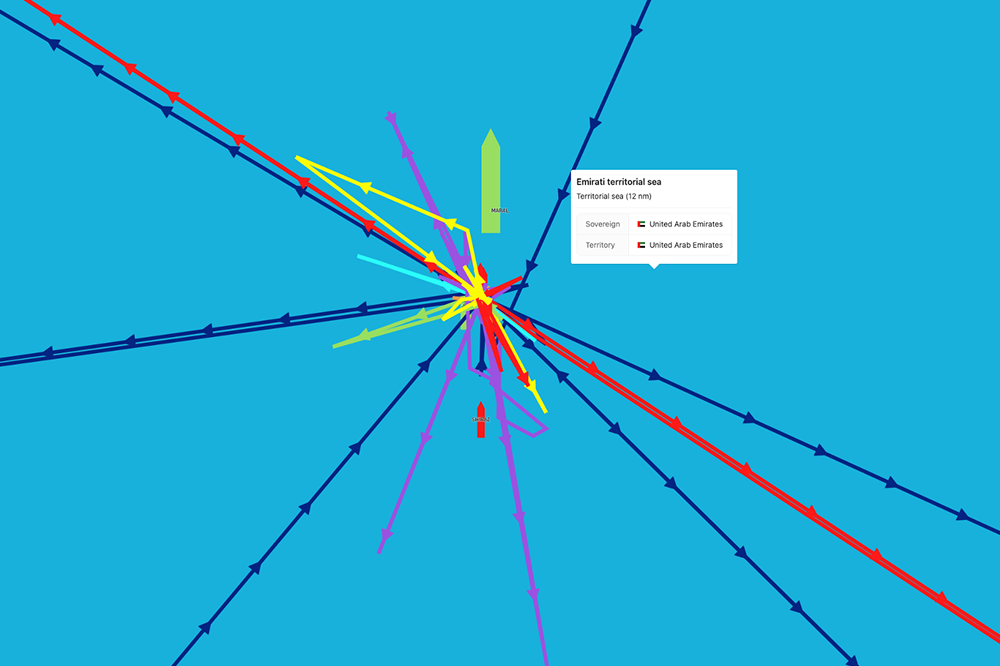

The Russian invasion of Ukraine has sent tanker rates soaring and especially on routes including Russian loading ports. Baltic Exchange’s Aframax TD17 between Primorsk to Wilhelmshaven jumped to above USD 170,000/day and the Suezmax TD6 between the Black Sea to the Mediterranean is quoted at more than USD 150,000/day. Recently earnings on these routes were estimated USD 5,000/day and USD – 3,000/day respectively. War can and will cause severe dislocations in trade and therefore, more often than not, shipping benefits from such situations. The first order effects as seen above mainly come about as supply is held back. Owners’ fear of the developing situation including being in breach of sanctions, which are now rapidly coming into place, lead to tonnage being withheld. Also, other vested interests such as insurers are either not offering to cover vessels or demanding huge premiums. The result being soaring rates. Those brave or foolish enough will receive a windfall, however, in today’s interconnected and transparent world it is very easy to identify the war profiteers. A quick view using Maritime Optima’s ShipAtlas can identify some of the vessels (see below illustration). The number of fixtures on Russian routes has therefore dwindled.

Source: ShipAtlas by Maritime Optima

Second order effects causing changes in trading pattern are already beginning to emerge. If oil cannot be sourced from Russia, buyers need to source it from elsewhere. The trouble is that new sources of crude or products will likely be further afield. The distance between Novorossiysk (Black Sea) and Lavera (France) measures 1832nm, while Bonny (Nigeria)- Lavera measures in excess of 4018nm. These dislocations are therefore beginning to protrude the tanker market. Even the AG-East VLCC market has begun to move. As is often said merely the fear of dislocations or bottlenecks has the potential to move markets.

Source: ShipAtlas by Maritime Optima

So far energy sanctions on Russia have not been introduced widely. As Europe (but also other parts of the world) are moving through an energy crises, EU authorities have made an exception for Russian energy (and Italy managed to include luxury items in the exceptions!). Some countries are beginning to move on energy sanctions, such as Canada, but do note that last time Canada imported a barrel of crude oil Russia was in 2019. Nevertheless, if Russian energy cannot find a home in Western countries it must either stay in the ground or find other outlets. It is rather unimaginative to speculate whether Russia could increase their exports to China, at of course a discount which compensates for increased shipping costs and other impediments, and also bypassing normal payment methods routines, such as the SWIFT system. For the shipping world this could mean again distances multiplying. Novorossiysk – Shanghai measures 8490nm. The conclusion is that despite some loss in volumes exported from Russia, the dislocations as seen in increased distances are and will have a tightening effect on the tanker market.

Russia’s oil and gas reserves are significant and according to BP’s Statistical review they amount to 6% of oil and 20% of gas global reserves. Europe is for example dependent on the Russian gas who provides 38% of pipeline gas. In comparison Norway provides 24% of pipeline gas. Several new routes to exporting gas from Russia have been invested in, such as Nord Stream 2 and South Stream. Lately, Russia has also pushed ahead with plans to build a pipeline to China as part of the Soyuz Vostok gas pipeline (the western part runs through the Ukraine). Another route which rises in importance is the northern shipping route. The northern shipping route has the potential to cut distances to markets in Asia by close to 33%. Activity along the northern shipping route has been increasing and in 2020 254 cargoes of LNG were exported from Sabetta/Yamal and 33 of these cargoes had destination Asia, with the large majority to China (source: Nord University).

The timing of the invasion was anything but precarious. As noted, the world economy is struggling with an energy crises. Without the invasion fundamental models of the oil market was pointing to Brent oil prices of USD90. The invasion has already added a premium of USD10. However, we estimate that if 2mbpd of Russian oil is withdrawn from exports, global spare oil production capacity will be at levels where the oil price traded well above USD100. Further, note that global oil inventories have already been drawn.

This situation will reverberate in several dimensions. Directly, and a consequence of the global need for oil, the Iranian conflict could be resolved. Evidently it is vital to address the oil market supply demand balance as it is a significant part and driver of inflation. US CPI is already moving above 7% yoy, not seen since the early 80ies. The trouble is that inflation is rapidly becoming embedded. As purchasing power of citizens is eroded wage pressure is emerging. Causes of the situation is well known. Covid induced massive fiscal transfers led to increased consumption and at the same time COVID restrictions led to disturbances in long industrial logistical chains. See for example the container market where we see that waiting days and distances travelled have increased, and also pushed rates up significantly. In terms of energy, government ESG policies have hindered investment in oil and gas. Further, the need for many other commodities in the renewable industries is far from dimensioned to demand. Inflation is therefore fast becoming part of the ESG transition.

Source: Maritime Optima

The global economy is in other words experiencing severe growing pains. Its capacity to grow given current policies is therefore less today than before COVID. The cyclical aspect means also that tightening financial conditions are overdue. With the arrival of the Russian invasion even more hard choices have arrived. Many central banks have already started tightening, but in the current situation they will be careful not to strangulate the global economy.

In terms of the tanker market, it has already benefited from the Russian invasion of Ukraine. When the invasion ends tanker earning will probably head back lower. While volumes may be somewhat lifted by OPEC increasing production through the year including possibly increased exports from Iran, we suspect that the available fleet capacity and productivity (see graph below for speed vs WS for VLCCs) will keep a lid on earnings.